That rumbling you hear is the tectonic plates shifting underneath the world of private equity.

“Tariffs have really thrown a monkey wrench into everything,” said Randy Schwimmer of Churchill Asset Management, an affiliate of Nuveen that finances US middle-market PE firms and their portfolio companies. “There’s a huge amount of uncertainty globally.”

At the SuperReturn private equity conference in Miami this week, dealmakers said the escalating trade wars sparked by US President Donald Trump have disrupted earlier expectations of an economic soft landing and PE recovery after several years of delayed exits and slow fundraising.

Even more fundamental market shifts that will play out over the next several years also demand attention now, warned Hugh MacArthur, chair of Bain & Company’s global private equity practice, who last week shared insights from the firm’s 2025 Private Equity Outlook.

PE firms are grappling with a wave of change that is set to fundamentally reshape the world of buyouts and private market investing, from the rising importance of wealthy individuals and sovereign wealth funds, to shrinking profit margins, to the merging of public and private markets, and increased competition for talent, deals and capital.

The available options, MacArthur says: Go big. Get acquired by someone who can. Or, differentiate yourself with specialized strategies for generating alpha.

The fundraising squeeze of the past few years in a high interest rate environment is only the most visible sign of a convergence of forces that are set to reshape the way fund managers large and small operate.

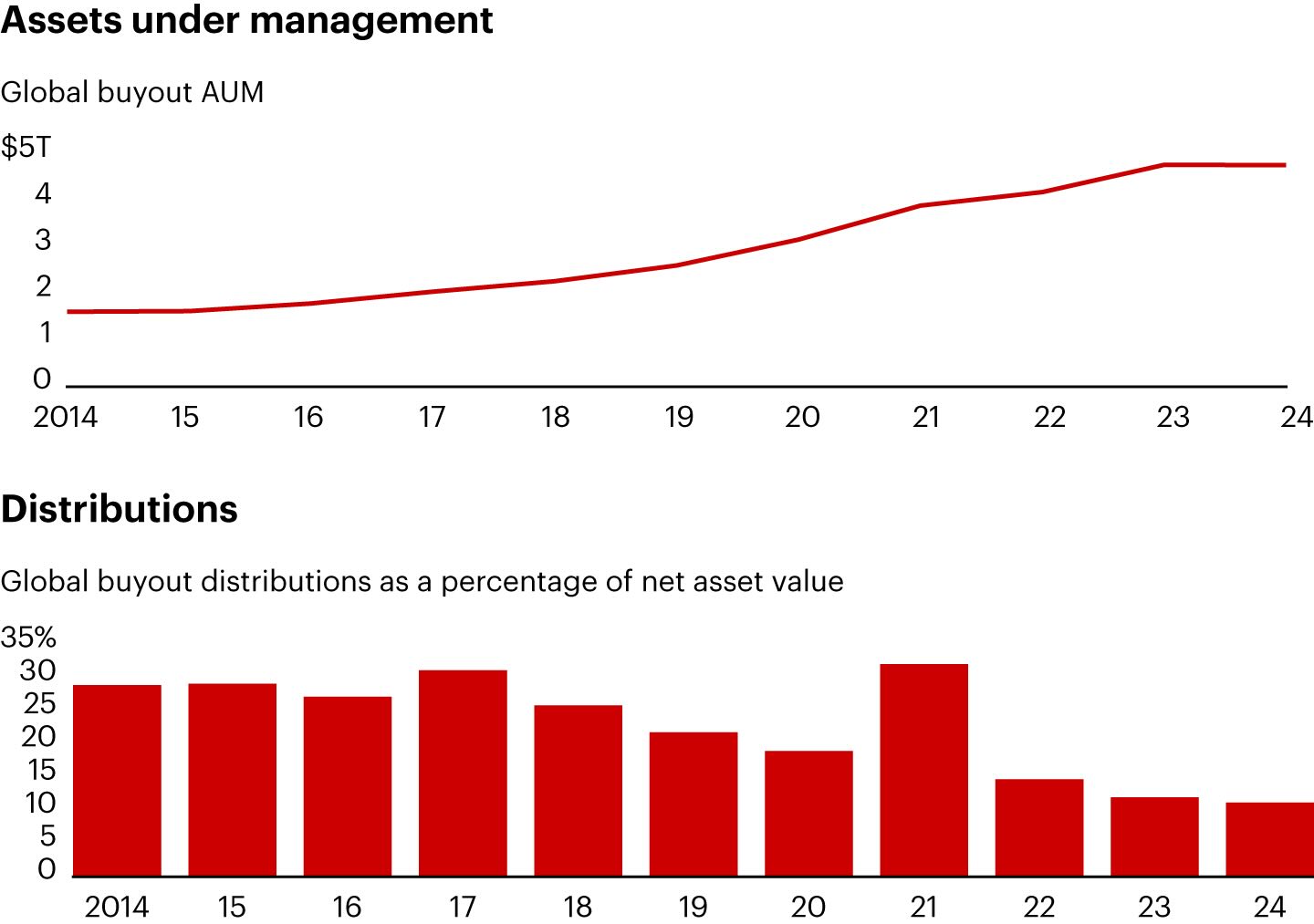

Distributions to investors have not kept up with growth in assets under management

Notes: Buyout category includes buyout, balanced, coinvestment, and coinvestment multimanager fund types; global buyout AUM through June 2024; global buyout distributions as percentage of NAV through Q3 2024, annualized. Sources: Preqin; MSCI; Bain analysis

“The next five or 10 years are going to be a different industry than it was 10 years ago, and a lot of these changes are going to require having a real strategy in order to adapt,” MacArthur said. “You’re going to have to have a differentiated strategy and the ability to execute.”

Standing out

The private equity industry has tripled in size in the past decade, to $4.7 trillion in assets under management, setting up fierce competition even as margins contract and liquidity challenges gum up the flow of capital. “It’s a little bit more of a zero sum game,” MacArthur said.

“If I’m a GP that looks a certain way, writes a certain check size, participates in certain industries, I may have to knock somebody else out that looks like me in order to get that allocation from that traditional institutional investor.”

That provides an opening for impact investors, who have shown they can deliver differentiated strategies and solid returns to stand out in a crowded sea of funds.

“Capital is flowing to the high end of the spectrum, and I think it’s ultimately to our collective shame, because great returns could be made that actually have higher impact on the society at large,” said Lafayette Square’s Damien Dwin on the sidelines of SuperReturn (hear Dwin for yourself on ImpactAlpha’s podcast, “Investing in working-class people and places”).

“We live in a world where, if you can produce 8-12% net returns, you’re very interesting compared to the stock market and other asset classes,” Dwin said. “If you could do that steadily, with low volatility, you’re making a huge impact. But that way of thinking – place-based, working-class people, working-class places – has eluded most GPs and asset owners.”

Bain’s 2025 PE Outlook charted the changing landscape:

Lack of liquidity

And you wonder why limited partners are antsy. Distributions to LPs as a percentage of their net asset value, or the value of their total holdings, was a mere 11% last year, compared to more typical expectations of 20% to 30% over a 3-5 year deal cycle. That’s down from 12% in 2023 and 15% in 2022. The last time the ratio was that low was during the Great Recession. The difference this time around: the industry is three times larger and there is no recession.

“Liquidity really is that bad,” says MacArthur. “That puts a real squeeze on LPS confidence in their ability to predict what they’re going to get back what return levels those are really going to look like, and therefore their confidence level in making commitments to new fund opportunities this year and next year.

Emboldened LPs have demanded fee concessions and co-investment opportunities, whittling away the traditional “two and 20” PE fee structure. Average net management fees fell by as much as half over the past decade and a half, according to Bain, and 30 cents of every PE dollar committed these days has no fees attached to it (for background see, “That (mixed) feeling when your LP co-invests in the sweet deal you’ve just negotiated”).

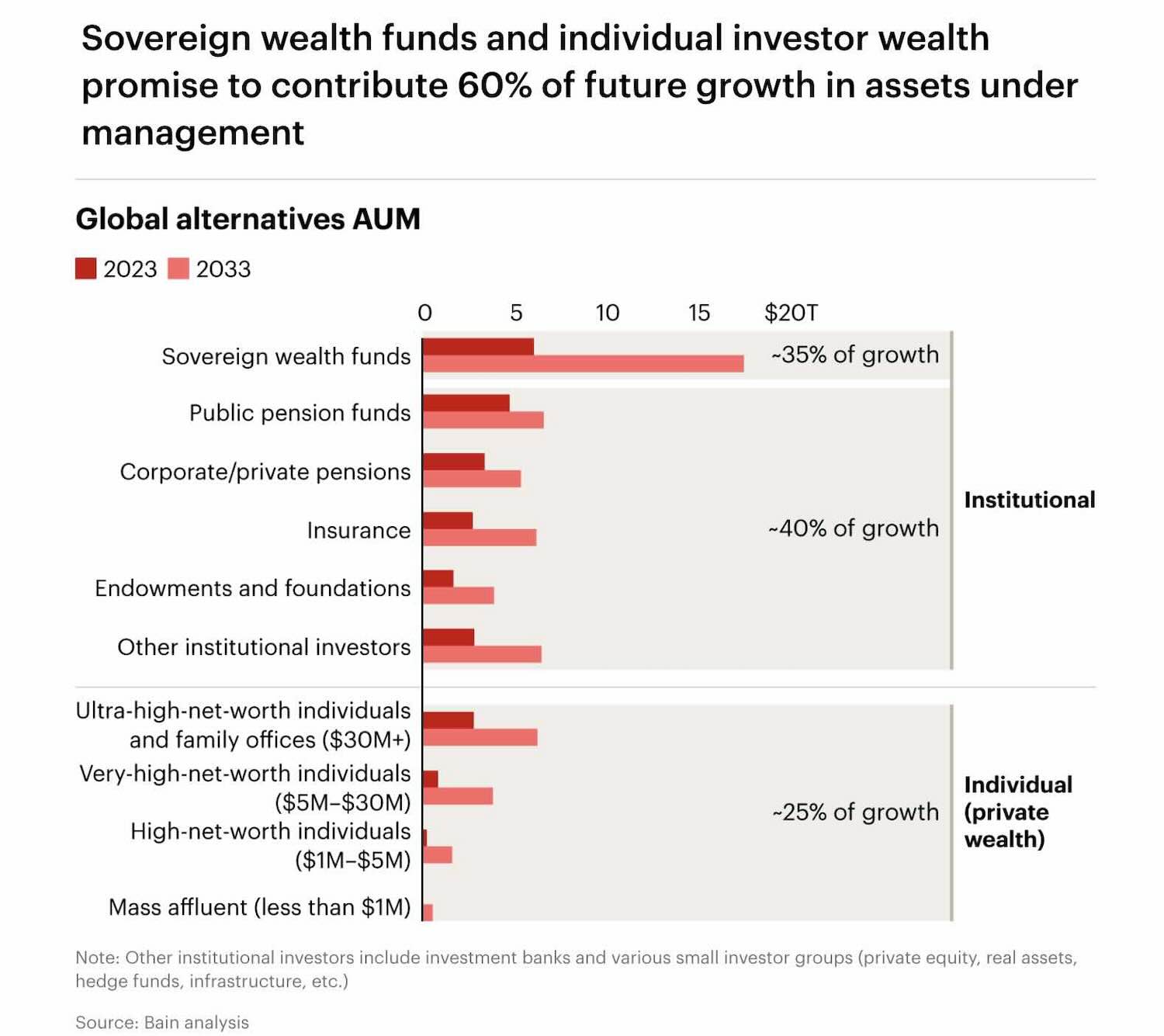

Retails and sovereigns drive growth

Institutional investors have been the bedrock of PE for years. But there are new kids on the block. Bain expects sovereign wealth funds and private wealth to drive 60% of growth in assets under management over the next ten years. Sovereign wealth funds, in particular, will be “the single largest source of dollars coming into the industry over the next decade,” said MacArthur.

Similarly, individuals hold some 50% of total global wealth, yet most people have few, if any, private equity investments. As the public markets have become increasingly concentrated in a handful of tech stocks, a case is being made diversifying the investment available to them.

“That white space and lack of allocation is going to drive huge growth,” said MacArthur.

The investor profiles are very different and will require new investments and strategies. Many sovereign wealth funds are enormous and need to write mega-checks, requiring funds to have a certain scale to play.

The private wealth market, in contrast, is characterized by a high volume of smaller investments, necessitating a beefed up staff to tap into the opportunity, as well as new products and partnerships tailored to that market. In addition to family offices, private equity funds are eyeing the mass affluent and even the $12 trillion or so held in retirement accounts as policymakers signal a loosening of securities rules.

MacArthur warns that reaching these new investors will raise the cost of capital for funds, further squeezing margins.

Public-private

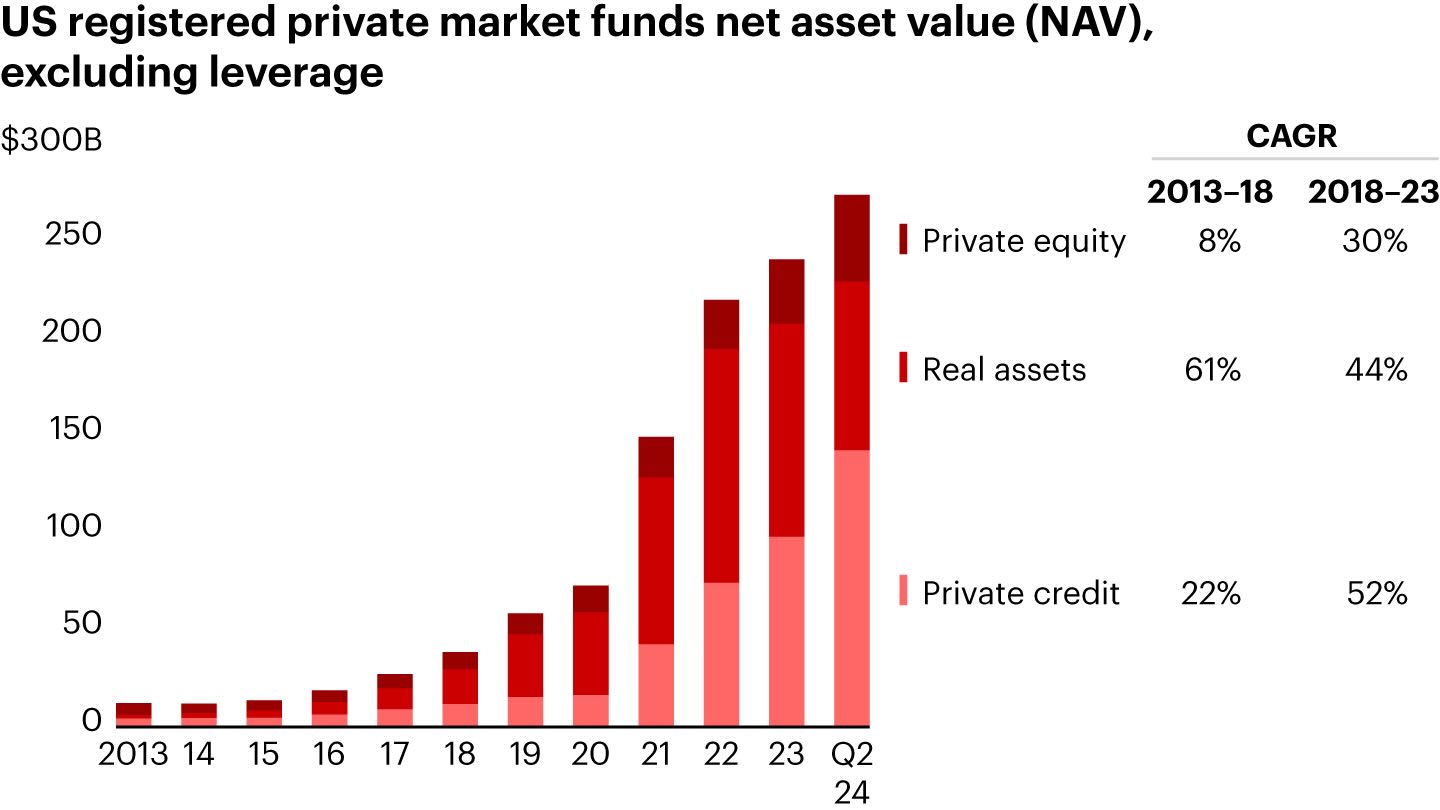

The growth prospects for the private wealth market are driven by an increasing blurring of the lines between traditional public market and private markets. Giant asset managers like BlackRock, Vanguard and Franklin Templeton have been tiptoeing into alternative investments to boost their margins and offer clients more diversification.

Semiliquid assets aimed at retail investors have shown strong growth over the past decade

Notes: Excludes private and finite nontraded BDCs and finite nontraded REITs; NAV for BXPE and K-PEC as of Q3 2024; NAV for nontraded REITs calculated by multiplying shareholders’ equity (SE) by a NAV/SE ratio of 1.35; ratio calculated using the average fraction of SE relative to NAV for two representative funds (BREIT and Starwood REIT)

Sources: Company websites; Internal Fund Tracker; Tender Offer Funds; Bain analysis

BlackRock, for example, snapped up Global Infrastructure Partners last year as well as private markets data provider Prequin, and is creating new products aimed at retail markets. It’s also readying new alternative products for retirement investors.

“We are seeing institutions worldwide blend public and private markets, and in many cases, it’s been a great investment,” said BlackRock’s Larry Fink said at a retirement summit it sponsored last week.

At the same time, traditional private equity players such as Apollo and Blackstone are banking on a likely shift in rules that would allow retirement plan sponsors to offer alternative investments. Blackstone’s retail-focused buyout fund, BXPE, has been scooping up cash.

To appeal to a more mass market crowd, PE players will have to create more liquid products and lower their cushy “two and twenty” fee structures.

Haves and Have-nots

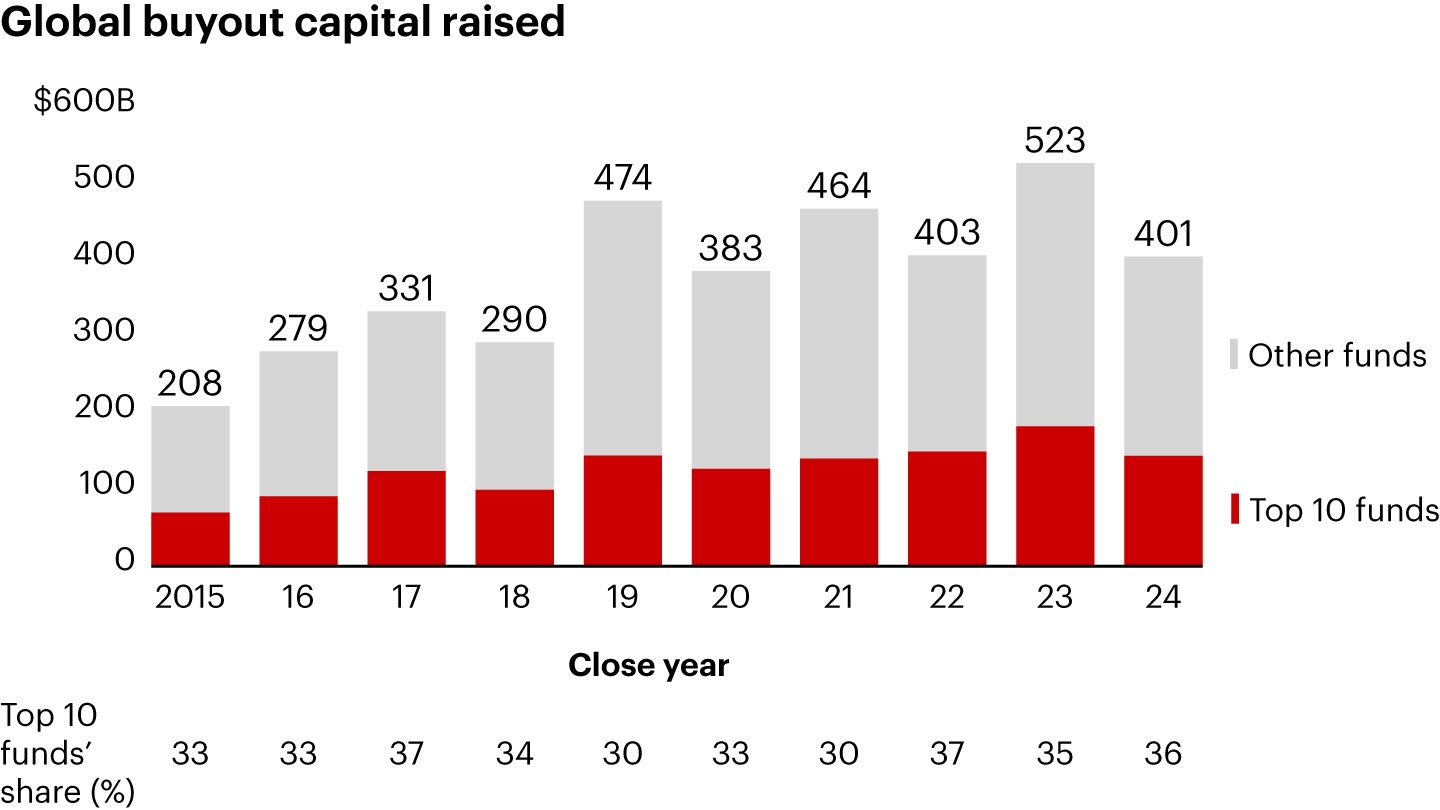

Fundraising was down for the third straight year, by 23%. Only infrastructure and direct lending bucked the trend. The dismal showing marred otherwise positive performance for exits, deal volume and deal value, all of which rebounded in 2024. Fund-raising is a lagging indicator for deal activity.

The top 10 funds typically account for 30% to 40% of all buyout capital raised

Notes: Top 10 funds defined as the largest 10 funds raised by value in a single year, independent of other years’ fund-raising levels; includes closed-end and commingled funds only; buyout category includes buyout, balanced, coinvestment, and coinvestment multimanager fund types; includes only those funds with final close data; excludes SoftBank Vision Fund

Sources: Preqin; Bain analysis

The number of fund closes fell to 366, levels not seen for a decade, when the industry was one third the size it is today. “That means it’s brutally difficult out on the road,” MacArthur noted. Of funds that managed to reach a close, more than a third were in the market for more than two years.

It’s increasingly a tale of two PE realities, with top performers pulling away from the pack. Since interest rates began to rise in 2022, the number of managers closing a fund has plummeted by 45%, even as average fund size rose.

Top quartile performers raised funds that were 50% larger than their predecessor funds, compared to a mere 0.4% boost for the bottom quartile. The time to raise a fund actually fell slightly for top performers, to 9.5 months, while nearly tripling for laggards to 33.5 months.